Open House

008: The 2025 Housing Crisis and America’s Broken Market

Introduction

Industry: Real Estate

Companies: XLRE BAC C GS WFC

In 2008, as a 16-year-old high school sophomore, my world revolved around what felt like life’s biggest concerns: cars, friends, and girls. College and the future were just distant worries overshadowed by the simple joys of growing up in Charlotte, NC. Back then, the city still had the feeling of a smaller, tightly woven community, and for families like mine that were rooted in banking, life felt secure. The economy had seemingly found its footing after the dot-com bust, and in a city that housed financial giants like Bank of America and Wachovia (which Wells Fargo would acquire by year’s end), job stability was a given. At least, that’s what we believed. Too young to grasp the weight of what was unfolding, I watched from the sidelines as the financial world cracked beneath the surface. The 2008 bailouts were just headlines to me, abstract policy decisions with no immediate consequence. But the aftershocks of that crisis didn’t just rattle Wall Street. They fractured the very foundation of real estate, creating fault lines that would take decades to fully emerge.

There is a downloadable PDF of this writeup found HERE

Be sure to check out our podcast HERE

Abstract

The 2008 financial crisis was a global economic disaster that sent shockwaves through the U.S. housing market, wiping out jobs, savings, and home values. While the recession eventually faded from headlines, its ripple effects never truly disappeared. Now, as we enter 2025, people are feeling more “priced out” of life than ever, particularly when it comes to homeownership. The soaring cost of starter homes isn’t just a financial hurdle. It’s a generational crisis with far-reaching economic and social consequences. This article will explore how the aftermath of 2008 set the stage for today’s housing affordability crisis, the impact on future generations, and what it means for industries and society as a whole.

How Much Does Happiness Cost

A poll by The Harris Group revealed a striking disparity in income expectations across generations, with Millennials standing out as a defining outlier. While Gen Z, Gen X, and Boomers reported needing an annual income between $124,000 and $130,000 to feel happy, Millennials estimated they would need $525,000, almost 4x the number of other generations. This gap highlights the unique financial pressures faced by Millennials who, now in their late 20s to early 40s, are facing the brunt of rising costs in nearly every aspect of life.

Unlike previous generations, Millennials are navigating a financial landscape led by skyrocketing home and auto prices, tuition debt, and persistent inflation. Many are at the stage of life where they are trying to buy homes, raise families, and build financial security. With homeownership long seen as a primary path to wealth-building, the significant rise in real estate costs has forced many Millennials to either delay purchasing a home or stretch their finances to unsustainable levels just to enter the market.

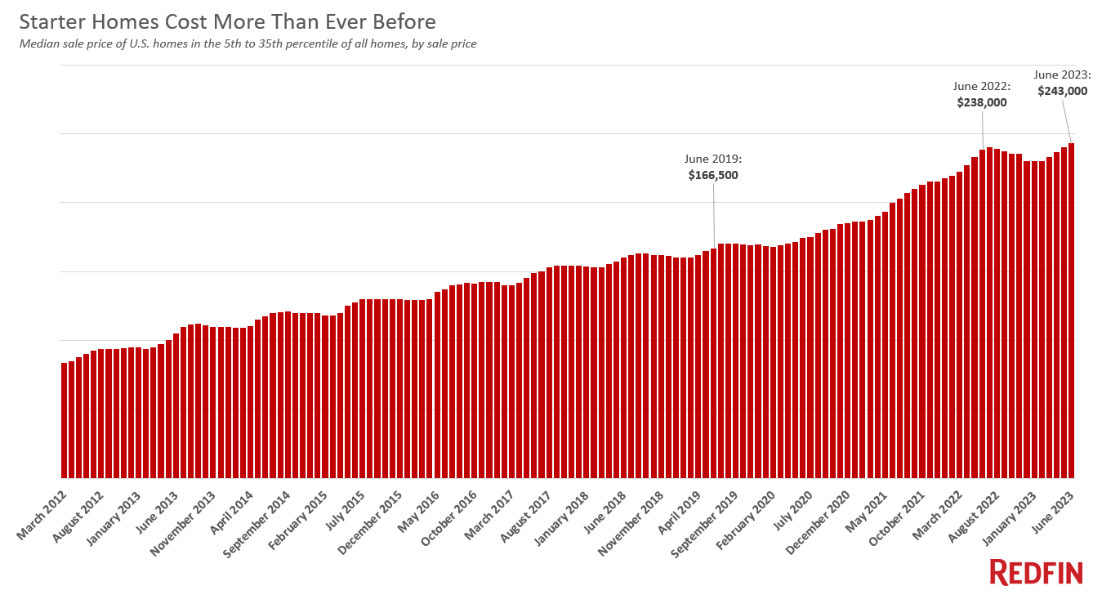

At the core of this financial strain is the disappearance of the affordable starter home. As home prices continue to soar, far outpacing wage growth, what was once a reasonable first step into homeownership has now become a unattainable for the majority. Unlike previous generations who could enter the market with modest incomes, Millennials are facing a stark reality where even a six-figure salary may not be enough to secure a home.

The Decline of Starter Homes

For this analysis, I will focus on a specific city and data point that could then be used as reference for the broader industry. Think of hotspots like Austin, TX, Nashville, TN, Columbus, OH, etc.

The cost of starter homes in Charlotte, NC, has skyrocketed over the past several decades, making homeownership increasingly out of reach for first-time buyers. In 1970, the average home in the area cost just $16,300, while the median family income was $9,564. However, the landscape shifted dramatically following the 2008 financial crisis and set the stage for the affordability challenges of today.

By 2011, the price of a starter home had climbed to $47,540. Between 2011 and 2018, prices rose at an annual rate of more than 16%, reaching $140,000 by 2018. This rapid increase outpaced wage growth, making it harder for buyers to save for a down payment, secure financing, or compete in an increasingly competitive market.

More recently, the trend has only worsened. As of November 2024, the median home sale price in Charlotte hit $423,500. This is 60% increase since 2019. With home prices rising faster than incomes, the dream of homeownership has become increasingly elusive, particularly for Millennials and Gen Z buyers. The sharp rise in starter home costs reflects broader economic trends, including supply shortages, rising construction costs, and inflation, leaving many to wonder if affordable entry into the housing market a thing of the past is now. But the question that must be answered is:

“Why is this actually happening?”

The answer has a trail of breadcrumbs back to 2008.

Golden Handcuffs: Expired

It’s 2005, and Christmas is just around the corner. Bank of America stock has fully rebounded from the Dot-Com bubble burst seven years prior, and confidence in the markets is strong. For bank employees, the holiday season brings more than just festive celebrations, it means year-end bonuses. As had been tradition across the industry, Bank of America rewarded employees with stock options, a lucrative perk that could significantly boost employee earnings. For those unfamiliar, a stock option is a financial incentive that gives the owner, in this case the employees, the right to purchase company shares at a predetermined price (known as the strike price) within a set time period. If the stock price rises, the employee can buy shares at a discount and potentially sell them for a profit.

But what happens when that stock price drops? As the 2008 financial crisis unfolded, bank stocks collapsed, wiping out the value of these once-promising incentives. Financial institutions that had seemed unshakable saw their stock prices nosedive, most institutions losing over 90% of their value or going bankrupt. A majority of these bank employees had factored these stock options into their long-term financial planning but were forced to watch from the sidelines that as their futures turned into worthless paper. And the worst part? Many of these options had expiration dates. Even as the markets eventually rebounded, employees who hadn’t been able to exercise their options before the downturn were left with nothing.

Except one thing… their homes.

The New Retirement Vehicle

In the aftermath of the 2008 financial crisis, the homes of many bank employees became a large percentage of their net-worth. It wasn’t just the bank stocks that had plummeted, home prices also fell sharply, leaving many people trapped in a "no man’s land" with little option but to ride out the storm. For most, their only recourse was to hold tight and wait for stabilization, a period marked by bailouts, mergers, and government intervention. While these measures eventually helped the economy recover, the emotional toll on individuals, especially those whose futures had been tied to their investments, was immense. Some employees would never set foot in a bank again, carrying the bitterness of losing their financial security. Meanwhile, others were absorbed into larger firms, marking the end of an era for many smaller banks.

As the economy stabilized, a significant shift occurred: those in the 25-50 age range in 2005, who had seen their retirement savings wiped out, found themselves with the bulk of their net worth tied up in their homes. Over the next 10 to 20 years, home values skyrocketed, and their homes became retirement vehicles. This generational shift played a key role in the growing shortage of starter homes. What used to be the predictable cycle of: new families buying a starter home, then downsizing once their children moved out, has now been disrupted. Rather than selling their homes, many in this generation chose to hold onto them as the market value continues to climb. Selling and then buying a smaller home in the same area now meant spending the same or even more money, something that was simply unfeasible. The result was a tight housing market where the traditional flow of homes became stagnant, further contributing to the scarcity of affordability.

But Wait… There’s More

There are a couple of other relevant, current factors happening right now that are worth mentioning:

Labor Workforce: Deportations have disrupted both the labor force and demand for housing.

Interest Rates: The Federal Reserve’s recent moves to combat inflation have led to higher mortgage rates, which have priced out a large portion of buyers.

Tariffs: Tariffs on building materials such as lumber, steel, and concrete have added another layer of complexity to the housing market.

Individually, these factors shouldn’t be much of an issue, because they would be counterbalanced by other real estate tailwinds. But they are now all swirling at once, which has created significant risk for implosion. In the years following COVID, many people increased their risk tolerance in an attempt to keep up with a rocket-fueled market that was pushing historic returns. And the sacrifices they made were far more than monetary.

Social Implications

As the cost of living continues to rise, young adults are increasingly delaying life’s milestones, choosing to focus on securing a stable financial future rather than committing to long-term relationships or family planning. This shift has profound social implications. The most concerning, however, is the decline in birth rates, a trend that has been observed since the 2008 financial crisis. This demographic shift suggests that as financial insecurity grows, so does the unwillingness to plan for a family.

While this shift may offer short-term economic benefits, it raises significant questions about the long-term social implications. A generation more focused on financial success than on relationships may face an enduring redefinition of what it means to build a future. One that could come at the expense of personal connections and community development.

Conclusion

I often find myself wondering: what if banks had paid cash for bonuses instead of stock options? Would the housing market have experienced the same massive disruption, or would the generational transfer of wealth have been more seamless? We will never know the answer. But, history has left me with this opinion:

I think it’s too late to correct what has been done. The financial crisis in 2008 created fault lines, and only one earthquake has happened so far. There is a chance to mitigate the size and scale, but at this rate, in a world where people ignore reality and scroll endlessly on video reels, it feels inevitable that we will face a harsh reality like many did in 2008. It’s like the famous scene in the movie “The Matrix”. Blue pill or red pill. Many have already chosen the blue pill. Personally, I will be waiting for a reason to purchase a new home. Without a significant discount to the asset price or a decrease to interest rates, there is no reason to lock up funds.

I’d like readers to consider this:

Recent data shows that roughly 55% of "peak boomers" are planning to retire within the next five years. This is the largest number of Americans ever to reach retirement age in history. To put in perspective: over the next three years, more than 11,200 Americans will turn 65 each day, adding up to over 4.1 million retirements per year from 2024 through 2027. The big question on my mind is: What happens if these homeowners don’t sell? If their homes are passed down to their children, many of whom, at current rates, may not have children or even a significant relationship. What kind of ripple effect will this have on the market? Will we see an even tighter housing supply, or will the market be flooded with demand once these properties change hands?

Both scenarios point to the potential for a major shift in the housing market. If the supply remains tight and demand grows, we could see a housing bubble that continues to inflate, creating an even more dangerous situation. Whatever happens, the future of the housing market is uncertain, but one thing is clear: This ongoing tightness, fueled by the reluctance of a generation to let go of their homes, has created the perfect storm.

There is a downloadable PDF of this writeup found HERE

Be sure to check out our podcast HERE

Very nice Dan