From Legacy to Leverage

003: The Trump Trade

Introduction

Tickers: JPM XOM CAT VMC X LMT

Industries: Energy - Financials - Industrials - Materials - Utilities

There is a downloadable PDF version FOUND HERE. If you missed last weeks PDF, I suggest taking a look for a more comprehensive read.

As Donald Trump takes office for his second and final term, his administrative policy agenda and political timeline carry significant implications for financial markets. With the clock ticking on a potentially limited window for legislative action, the focus will be on delivering bold reforms that could reverberate throughout the economy and stock market. Key policies and proposals that have surfaced in the last two days include historic tax cuts, new tariffs, and federal workforce reduction.

Trump’s ability to execute this agenda hinges on the 2026 midterms, which history suggests could shift power away from Republicans. This two-year window heightens urgency and market sensitivity to policy development. Investors will want to closely monitor legislative progress, geopolitical developments, and market responses as Trump seeks to solidify his legacy. This intersection of bold reforms and political constraints promise a period of heightened market activity, opportunity and uncertainty.

Abstract

The term "Trump Trade" describes the financial market's response to policy initiatives, statements, and broader economic trends under President Trump. Characterized by both significant market gains and increased volatility, the "Trump Trade" presents a mix of opportunities and risks that investors must navigate carefully. Looking forward, as new policies and trends emerge, the potential impacts on the stock market over the next four years demand a closer examination.

Opportunities

Further Corporate Tax Cuts and Deregulation

One of the hallmark initiatives of President Trump's administration was the Tax Cuts and Jobs Act (TCJA) of 2017, which reduced the corporate tax rate from 35% to 21%. This move created and stimulated corporate investment and economic growth. For investors, the tax cuts translated into immediate earnings growth for corporations, driving stock prices higher.

While TCJA is set to expire at the end of 2025, there is little concern as to any dramatic changes that will take place upon expiration. Banking ($XLF) and Energy ($XLE) companies should continue to be among the biggest beneficiaries. If themes of TCJA remain intact, and possibly furthered, financial institutions will see improved margins, and energy firms will continue to benefit from relaxed environmental regulations, which lower compliance costs and encourage expansion in oil and gas exploration.

Indices, such as the S&P 500 and the Dow Jones Industrial Average, surged to record highs following the tax reform announcement in 2017 and have all but continued that trend since. Over the last 7+ years, two of the more notable stocks have been JPMorgan Chase ($JPM) and ExxonMobil ($XOM). Both have seen substantial appreciation during this period as a result of TCJA. If similar policies are expanded or extended, sectors such as finance ($XLF), and energy ($XLE) are expected to see continued growth.

”Drill baby, drill”

President Trump lost no time in pushing forward his oil and gas strategy at his inauguration on Monday. Having taken the oath of office, the president declared an "energy emergency" in the U.S., and repeated one of his successful election campaign slogans: “Drill baby, drill".

Trump has urged U.S. oil and gas companies to ensure America's energy security and economic prowess, stating: "We are a rich nation. It’s that liquid gold under our feet that will help us ensure that we keep things that way... America will be a manufacturing nation once again. We sit on the most oil and natural gas of any nation on earth, and we're going to use it."

Infrastructure Spending Plans

President Trump’s promises of significant infrastructure investment have long been anticipated as a potential catalyst for economic growth. Construction, materials ($XLM), and industrial manufacturing ($XLI) companies are poised to benefit from increased government spending on roads, bridges, and airports. Companies like Caterpillar ($CAT) and Vulcan Materials ($VMC) have seen speculative increases in stock prices in response to these policy promises. While the proposals create optimism, delays in implementation and funding debates mute some of the expected impacts. The next four years could bring renewed efforts to prioritize infrastructure, creating opportunities in green construction and technology-focused upgrades to infrastructure.

Focus on Domestic Manufacturing

The "America First" economic strategy prioritizes reshoring manufacturing jobs and industries. Manufacturing ($XLM), Defense ($XLI), and Steel companies should experience further resurgence as tariffs on imported goods create a competitive advantage for domestic producers. Two examples of stocks that stand benefit from this type of focus are the United States Steel Corporation ($X) and Lockheed Martin ($LMT). With advancements in automation and technology, domestic manufacturing could pivot towards high-tech and renewable energy sectors, creating new investment opportunities.

Risks

Non-US Entities: Tariffs & Taxes

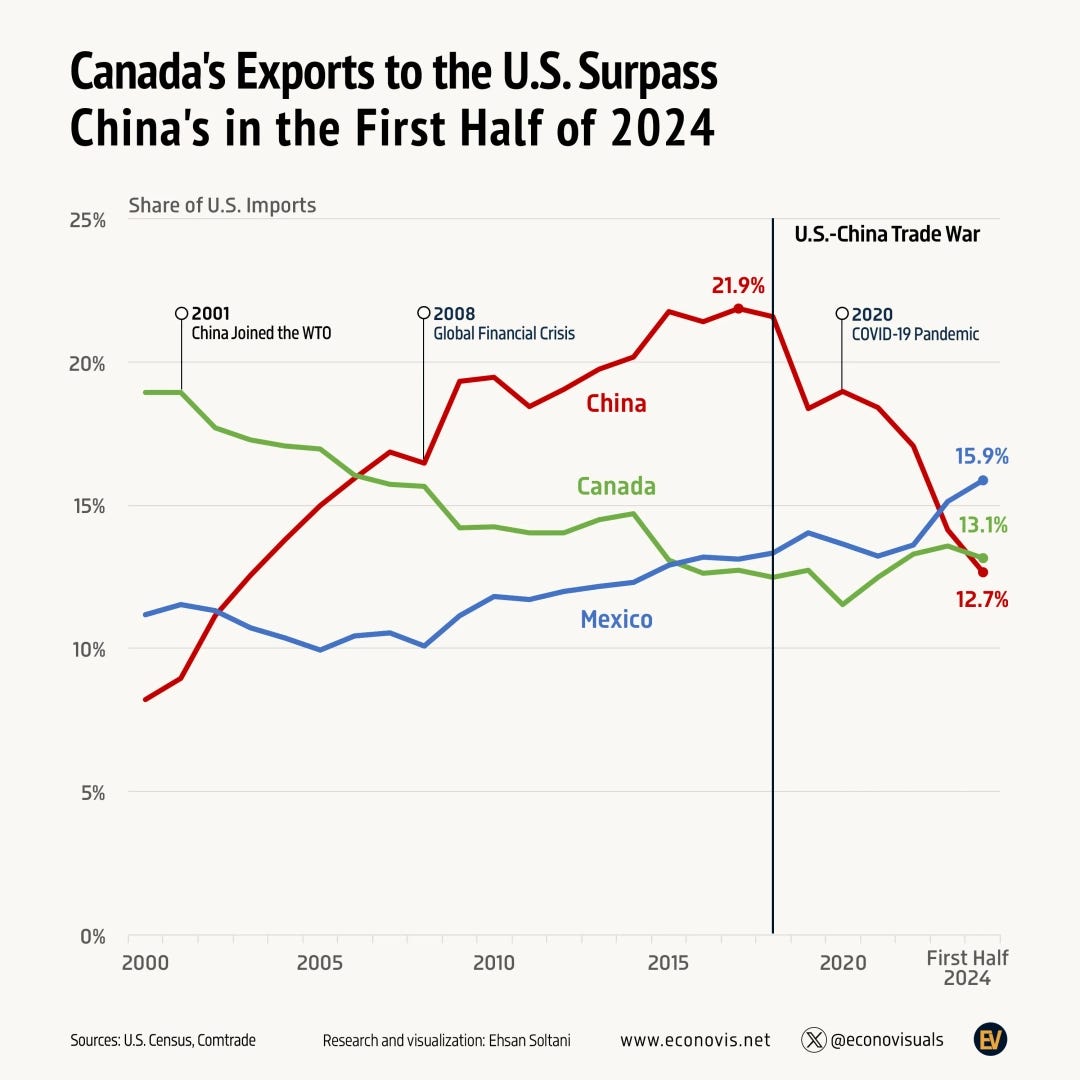

President Trump's approach to international trade is characterized by a focus on renegotiating trade agreements and imposing tariffs on imports from key trading partners, including China, Canada, Mexico, and the European Union.

The announcement of tariffs often triggers significant market volatility. During his first term, President Trump introduced an initial 25% tariff on Chinese goods, prompting retaliatory measures and creating uncertainty in industries heavily reliant on global supply chains, such as technology and automotive manufacturing.

Shortly after his inauguration, Trump continued this strategy, implementing a 25% tax on products from Canada and Mexico, along with an additional 10% tariff on goods from China. These measures are presented as tools to bolster the U.S. economy, safeguard domestic jobs, and increase tax revenues.

It is important to note, however, that approximately 40% of the crude oil refined in the United States is imported, with the vast majority sourced from Canada. Canada is also a critical supplier of natural gas and electricity to the U.S. This underscores the interconnected nature of North American energy markets and the potential implications of such trade policies. Market participants should keep their head on a swivel as the February 1st, 2025, deadline approaches for implementation of these taxes and tariffs.

Department of Government Efficiency

One of the most intriguing narratives of President Trump’s administration is the establishment and use of the Department of Government Efficiency (DOGE), led by Elon Musk and Vivek Ramaswamy. The selection of these two figures to oversee a department designed to reduce government spending and enhance efficiency adds a layer of irony to an already meme-worthy acronym.

But it’s not the memes or the high-profile leadership that are drawing the attention of investors. The pressing question for market analysts, particularly at SEBS, is: What impact will DOGE have on government contracting in 2025? Many Fortune 2000 companies depend heavily on the government market to drive consistent growth and deliver results for investors. This market includes U.S. federal agencies such as the Department of Defense (DOD), Internal Revenue Service (IRS), and Securities and Exchange Commission (SEC), as well as State, Local, and Education (SLED) entities.

As of 2024, the leading recipients of U.S. government contracts include well-known names such as Lockheed Martin Corp ($LMT), RTX Corp ($RTX), and Boeing Co ($BA). These companies, among others, collectively receive billions of dollars annually through federal contracts. Understanding DOGE’s potential impact on the government contracting landscape will be critical for industry stakeholders navigating this evolving space.

Since December we’ve seen companies like Palantir ($PLTR) and Anduril Industries collaborate with technology groups to pursue government contracts. These consortiums represent a more efficient and cost-effective approach to securing government deals. Elon Musk has already signaled that Pentagon spending and priorities will be key targets of the efficiency agenda. As a result, legacy vendors such as Boeing may face significant disruptions if they fail to adapt to evolving market strategies.

These shifts introduce considerable risks to industries and well-established companies that depend heavily on government contracts. However, the success of this transformation ultimately hinges on DOGE fulfilling its mandate effectively. In the search of long-term growth opportunities in this changing market landscape, it is important to assess the percentage of a company’s revenue derived from government contracts. Understanding this dependency offers critical insights into potential vulnerabilities and opportunities as DOGE reshapes the contracting ecosystem.

Conclusion

The next four years promise a renaissance in technology, culture, and governance, yet they will also be marked by heightened risks, including volatility, policy uncertainty, and geopolitical tensions. As new policies take shape, investors must stay vigilant, balancing optimism about growth opportunities with strategies to manage potential challenges. Emphasizing strategic diversification and focusing on long-term trends—such as technological innovation and sustainable infrastructure—will be crucial for successfully navigating this dynamic and evolving landscape.